The week started on a cautious note in Europe, but in a better mood for the US' tech-heavy indices. The Nasdaq 100 advanced more than 1% on Monday, with chipmakers leading gains. Broadcom, for example, jumped 3.7% after extending an agreement to provide new custom chips to Apple through 2031, while VanEck's Semiconductor ETF added 2% ahead of Samsung Electronics' earnings announcement today.

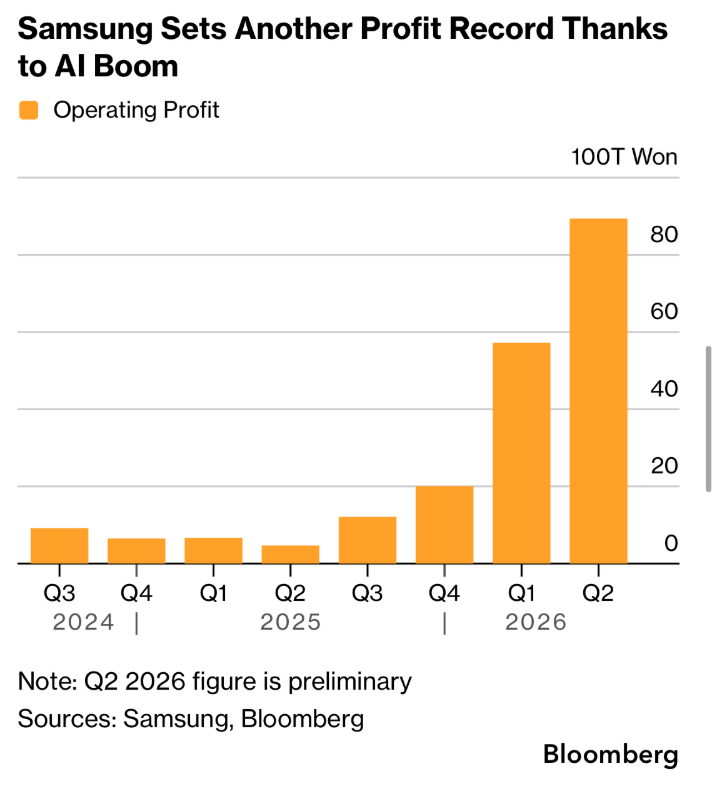

And the latter didn't go well. I mean, it did—looking purely at the numbers. Samsung delivered VERY strong – and stronger-than-expected – results. Its operating profit rose to nearly ₩90 trillion (the equivalent of $58bn), its quarterly profit surged 19-fold year-on-year and the profit margin for the memory chip business was around 80% – also showing the incredible pricing power the company has thanks to booming AI demand.

Yet, Samsung shares tanked 9% in South Korea after the results, pulling the Korean Kospi 8% down – yes, the index is down almost as much as a single company's stock – this is how overly dependent the Kospi is on the health of just two companies. Trading there was stopped again to give the market room to breathe!

Elsewhere, chip and related stocks across Asia pulled back sharply. Kioxia Holdings in Japan – a direct competitor to Samsung in the NAND flash memory business – lost more than 10%, while Tokyo Electron is down by 3.5% at the time of writing.

Whispering trouble...

How did this happen despite a decent earnings beat? The answer is that the real expectation—the so-called whisper number—was even higher than what analysts had pencilled in. The whisper number is the unofficial earnings target that circulates among investors, traders and portfolio managers ahead of a company's results.

Here is the catch. Whisper numbers always circulate. But in some periods, like during the dot-com bubble, these unofficial expectations become almost more important than Wall Street forecasts. When it happens, companies can beat analysts' estimates and still see their shares tumble simply because they failed to meet what the market had quietly convinced itself was achievable. Unsurprisingly, when valuations become stretched, investors stop asking whether earnings are good—they ask whether they are good enough to justify the price already paid. Everybody agrees—I guess—that a 19-fold profit increase is exceptional. But the stock price has risen more than sevenfold over the past year.

In summary, today's ugly reaction to exceptional Samsung earnings is a reminder that, in richly valued markets, meeting expectations is no longer enough; companies increasingly have to beat the whisper number as well. That is one of the classic characteristics of late-stage bull markets, when expectations begin to outrun fundamentals.

Oil faced to two opposite forces

European and US futures are looking cautious this morning, suggesting a pullback in today's session. Lower technology appetite is coupled with a slight rebound in oil prices on news that two ships have been attacked in the Strait of Hormuz.

The latter could hint at a possible re-escalation of tensions in the Middle East, which could in turn put fresh upward pressure on energy prices.

But for now, the oil market is being driven primarily by ample supply: the release of strategic oil reserves and tepid demand from China since the start of the Iran war led to oversupply in some key markets. And now, the tankers full of oil that had been waiting for months to leave the Strait of Hormuz are sailing through in search of buyers. There is so much oil at sea now that Saudi Arabia made a big cut to the price of its main crude for Asian buyers and started selling its oil at a discount to the Asian benchmark for the first time since 2020—the pandemic period when demand had dried up and oil prices briefly turned negative, remember?

So, oil markets are grappling with two opposing headlines this week: rising tensions in the Strait of Hormuz and Saudi Arabia's deep price discount to help the market absorb its oil more rapidly. I believe that the latter—the ample supply story—will outweigh the price action in the coming days, unless traffic through the Strait of Hormuz is jeopardised and/or the US-Iran peace negotiations take a sour turn. Until then, any price rebounds will likely meet sellers. For US crude, we will likely see strong resistance around the $70pb psychological level and then near $75pb, where the 200-DMA lies.

Today, in the absence of major economic data, markets will digest the ugly reaction to Samsung's earnings, the possibility of re-escalation in the Middle East and the potential implications for global risk appetite. The US dollar is stronger this morning, while gold is softer—a sign that the yellow metal is still moving in tandem with risk assets rather than exhibiting its usual negative correlation. Its hedging power has not fully returned yet.

The EURUSD is being offered above the 1.1450 mark, while the USDJPY eases below 162 on fears that speculative short positions may have become too stretched—hinting at the possibility of a sharp correction, especially in the event of direct FX intervention. According to the latest CFTC data, leveraged funds have not been this short the Japanese yen since 2007. Meanwhile, the Japanese 10-year yield consolidates above the 2.80% mark—still significantly lower than the US 10-year yield, which stands near 4.5% this morning. But the gap is closing with the rising risk that, at one point, Japanese investors will begin repatriating funds back home, potentially vacuuming up part of the roughly $10 trillion that Japan presently holds in foreign assets, including several trillion dollars invested in overseas bonds and equities. Even a modest shift of these funds back home could tighten global liquidity, lift overseas bond yields and put pressure on risk assets worldwide.

The last major episode that reminded investors of this risk came during the sharp yen carry trade unwind in the summer of 2024.

The content of this website is for informational purposes only and does not constitute financial advice. All opinions expressed are solely my own and should not be considered as recommendations to buy, sell or hold any financial instruments. Readers should consult a qualified financial advisor before making any investment decisions.

With love,

Ipek Ozkardeskaya