It’s the last day of the month and the quarter – the best quarter for global equities in the past six years according to Bloomberg, despite the Iran war, disrupted oil and fertilizer flows, and a spike in energy prices that led to a rise in global inflation expectations, which in some parts of the world resulted in interest rate hikes and, in others, more hawkish monetary policy. Regardless, global equities were boosted by the AI buildout. Of course, the indices with little AI exposure were left behind, and the rather narrow market breadth is raising a few eyebrows.

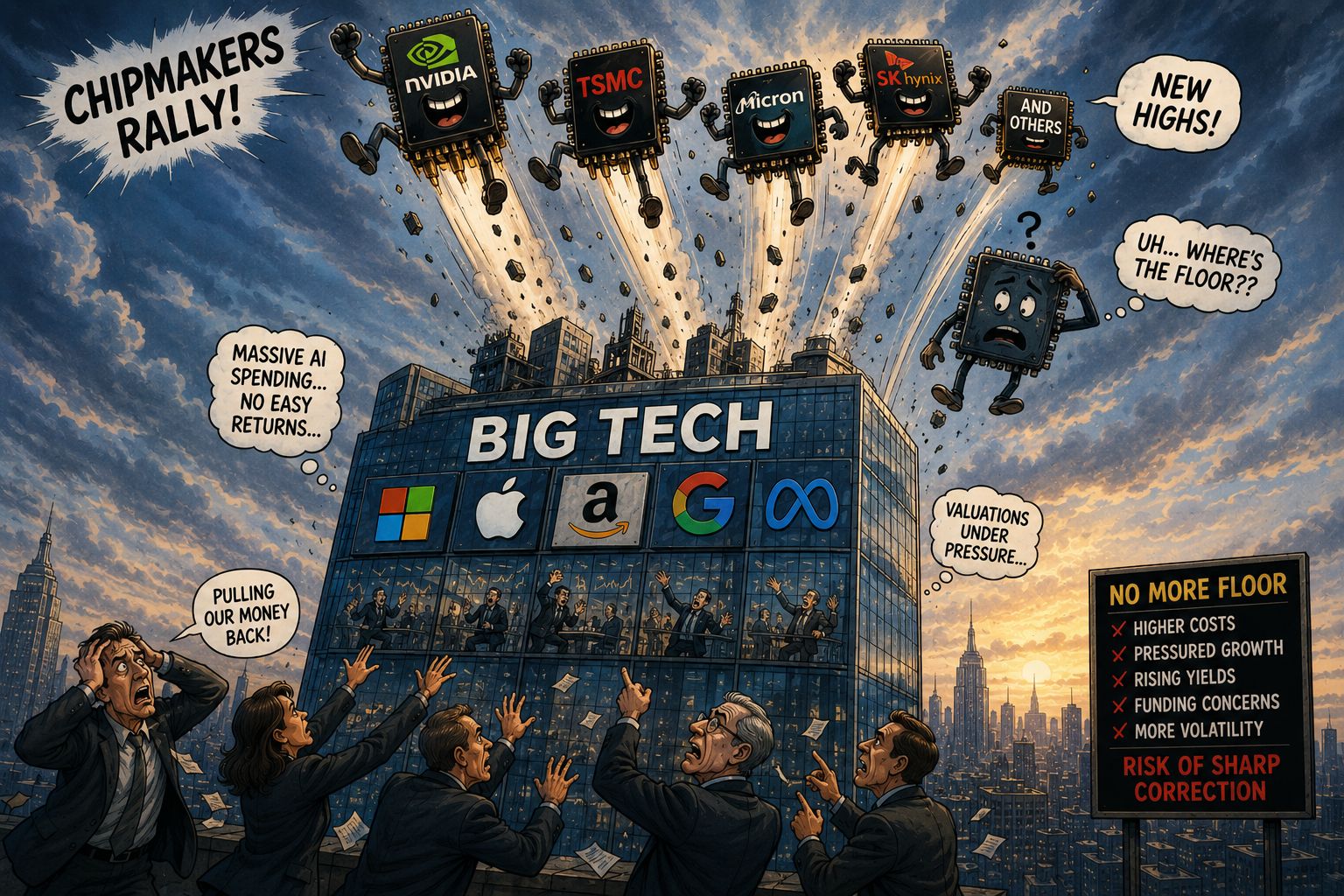

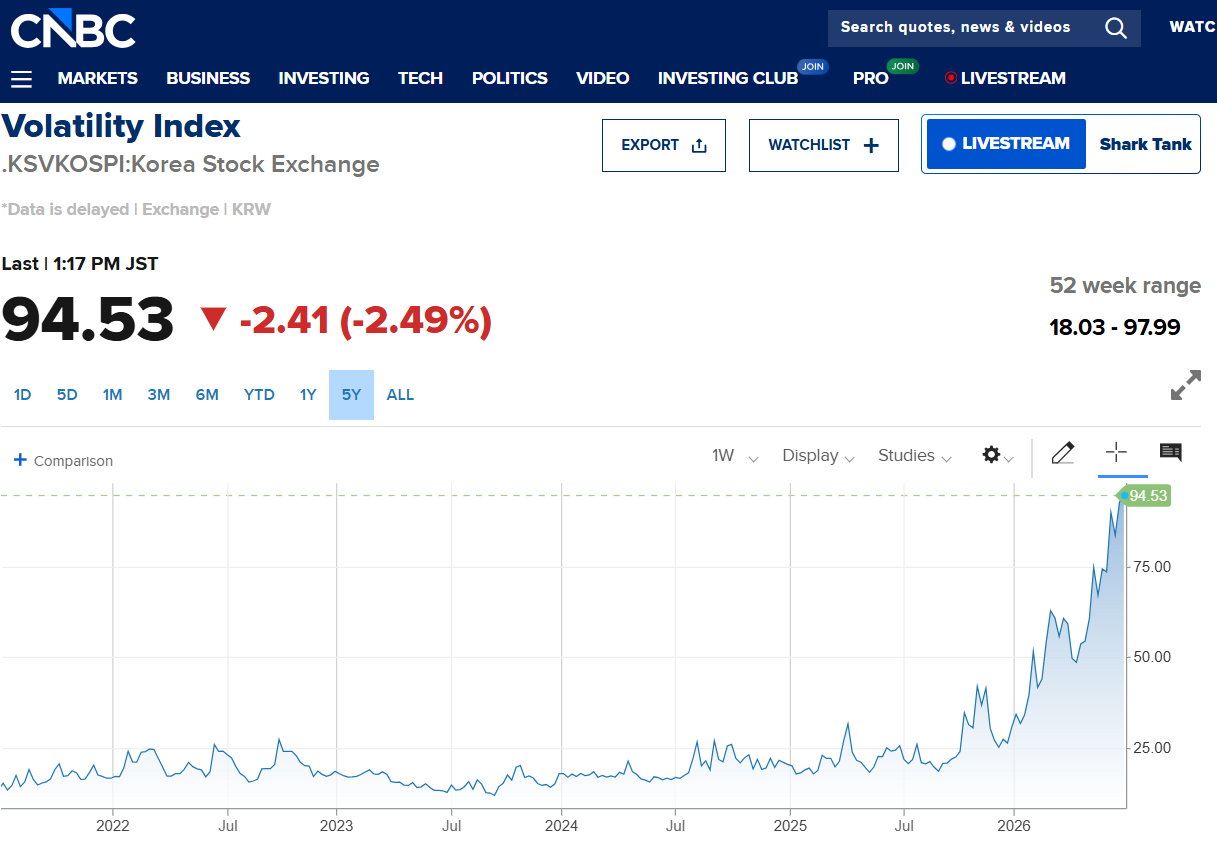

The rally continues despite eye-watering volatility in the Kospi index and unusually high valuations for chipmakers. The Korean Kospi index – which was slightly lower yesterday before the announcement of massive investment in new fabs – is up 2.40% today, the Nikkei is modestly higher, while US stocks, which started the week on a strong footing, are looking bullish judging by rising S&P 500 and Nasdaq futures.

What if Big Tech slows spending?

But not all tech stocks are performing well. The AI enablers – the beneficiaries of massive AI spending – are outperforming, while Big Tech – the companies spending heavily on AI infrastructure – are sputtering. The Magnificent 7 is down nearly 15% since the May peak, with Microsoft losing more than a third of its valuation since October last year. The AI and software giant is being pressured on both ends: on the one hand, its massive AI spending is displeasing investors; on the other, its software business is increasingly seen as being challenged by AI. It still has its cloud segment, which should continue to grow alongside AI adoption, but investors are heading for the exits.

Another stellar AI play, Google, is also down 17% since the May peak. Despite its Gemini model, TPU chips and data centre business – Google has everything to benefit from AI adoption – it is nevertheless being pressured by investors' reluctance to reward additional spending. Meta is down nearly 30% since last August because it neither has a leading AI model nor a clear strategy beyond overloading its social media platforms with AI-generated content, while Amazon is also down nearly 19% since the May peak. It, too, continues to spend heavily on AI infrastructure, including data centres and chips.

Do you see where I am going?

The massive AI spending from these so-called hyperscalers has allowed companies like Nvidia, Micron and their peers to deliver mind-blowing rallies over the past few months.

But investors are no longer happy with this spending; they are pulling their money back.

Hyperscalers still have the bond markets to finance spending for a while.

Then eventually, if funding becomes more difficult, they will slow down.

If Big Tech's massive AI spending slows – even a little – the future revenues currently priced in for the AI enablers will fall, and so will their valuations.

And the higher the yields, the greater the size of a potential correction.

In summary, I am not sure that the chip rally can continue without the precious support of Big Tech. If Big Tech sneezes, the whole supply chain will catch a cold.

Anyway, that's just an unpleasant thought.

Global macro

The good news is that US crude rebounded only slightly yesterday following the weekend tensions in the Middle East and is holding near $70pb despite another wave of conflicting headlines: Trump says the peace talks will resume in Doha today, while Iranian officials say they will not.

And the Middle East tensions do not matter much for global risk appetite as long as oil prices remain contained. They remain contained mostly because of oversupplied oil markets, thanks to historic strategic reserve releases and oil tankers sailing through the Strait of Hormuz under the radar.

The problem is that a US-Iran peace deal may not be as easily inked as hoped, traffic through the Strait could slow again, and this time strategic reserves will be alarmingly low to reassure investors in the event of a prolonged conflict. As such, the $70pb level could act as a floor beneath the latest retreat in oil prices. Upside pressure could flare up if this week does not bring any material progress in US-Iran negotiations, which could keep bond investors on edge, push yields higher and apply renewed pressure on global financial markets in the coming quarter.

The question then becomes: who would carry the market higher?

The US dollar gains field

Today, the US dollar is better bid against most major currencies and metals:

- The EURUSD has retraced yesterday's gains and is pushing back below the 1.14 mark.

- The GBPUSD is dealing with political uncertainty as Andy Burnham lays out his plans for how he would put Britain back on its feet while maintaining fiscal discipline.

- The USDJPY has spiked above 162 as everyone is holding their breath to see when Japanese officials intervene. The most likely reason why they have not done so is the gradual pace of depreciation and the overwhelming dominance of the US dollar. Today, the yen is weakening slowly because the interest rate differential between the US and Japan remains firmly in favour of the US dollar, and the US dollar is broadly bid. Intervening now would change nothing about the underlying market direction, but would cost dearly. Unless we see an aggressive selloff in the yen, the Japanese authorities seem willing to remain on the sidelines.

- Gold is gently clearing the critical $4’000 support. The yellow metal has now entered a medium-term bearish consolidation zone (below $4’115, the major 38.2% Fibonacci retracement of the October 2023 to January 2026 rally), suggesting that a deeper pullback is possible. The next target for the gold bears stands at $3’680 per ounce, corresponding to the long-term uptrend base and the 50% retracement. For long-term investors, gold remains an attractive asset. Many central banks sold part of their gold holdings during the last quarter to offset the energy price spike, and they will eventually need to replenish those reserves. The question is: at what price?

The content of this website is for informational purposes only and does not constitute financial advice. All opinions expressed are solely my own and should not be considered as recommendations to buy, sell or hold any financial instruments. Readers should consult a qualified financial advisor before making any investment decisions.

With love,

Ipek Ozkardeskaya