Yesterday’s weak US jobs data echoed positively across US government bonds and somehow neutralized the negative mood across technology stocks.

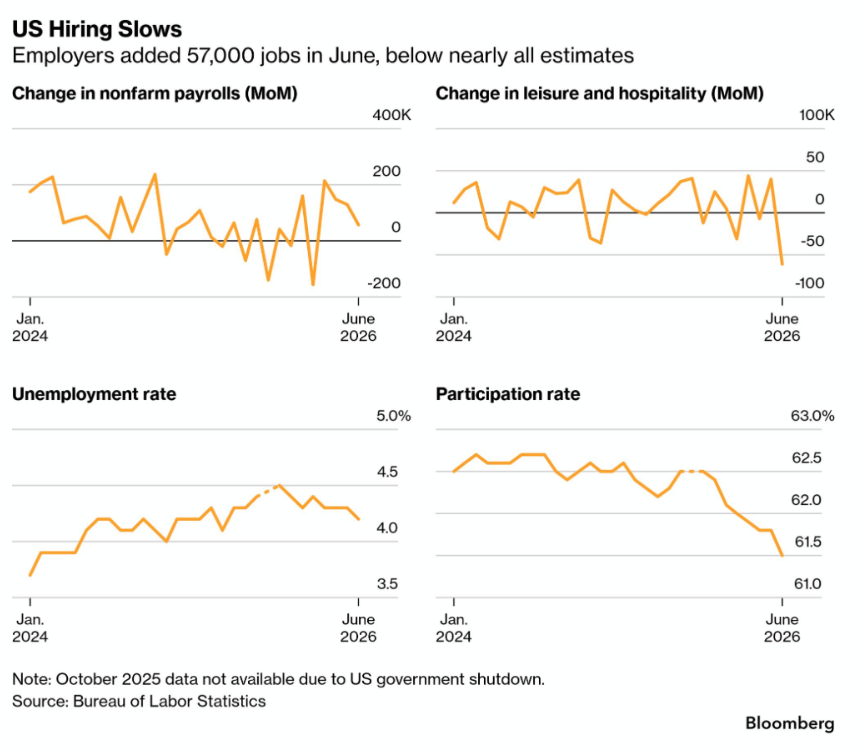

The US economy added 57,000 new nonfarm jobs in June, the past two months’ readings were revised lower, wage growth came in line with expectations (0.3% m-o-m and 3.5% y-o-y), while the unemployment rate fell to 4.2%. But that was due to a decline in labour force participation.

Overall, the data looked soft enough to encourage the market to trim Federal Reserve (Fed) rate hike expectations for this year. The market still expects the Fed to hike once this year—with a little more than a 50% chance of that happening as early as September. The US 2-year yield is softer but holding above the 4.10% mark, as US crude rebounds slightly from yesterday’s dip to $67pb but remains calm near the $70pb level, with no major headlines on the peace negotiations front. There is more news about increasing oversupply in key markets, and tens of millions of barrels of Iranian oil sailing without a preset destination, than worries about supply shortages.

As such, the softer US jobs data, combined with a sustained decline in oil prices, sent the US dollar lower against most major currencies yesterday. The EURUSD recovered and is consolidating near 1.1445, Cable approached the 1.34 mark, while the USDJPY fell nearly 1% to 160.62 yesterday. The move was also supported by Katayama’s comments that the authorities remain ready to intervene directly to slow the yen's selloff. Gold jumped to $4’195 per ounce from below $4’000 earlier this week, as softer yields reduced the opportunity cost of holding the non-interest-bearing metal.

Overall, the latest weakness in US jobs data and softer inflation expectations may reset Fed expectations to a slightly less hawkish stance. But it will ultimately be up to the inflation data to determine whether that shift continues. As such, we could see the US dollar consolidate its latest gains, with limited upside for gold and major currencies in the coming days. The next US CPI update is due on 14 July and will determine whether Fed expectations soften further, enough to neutralize current rate hike expectations.

Tech versus the rest

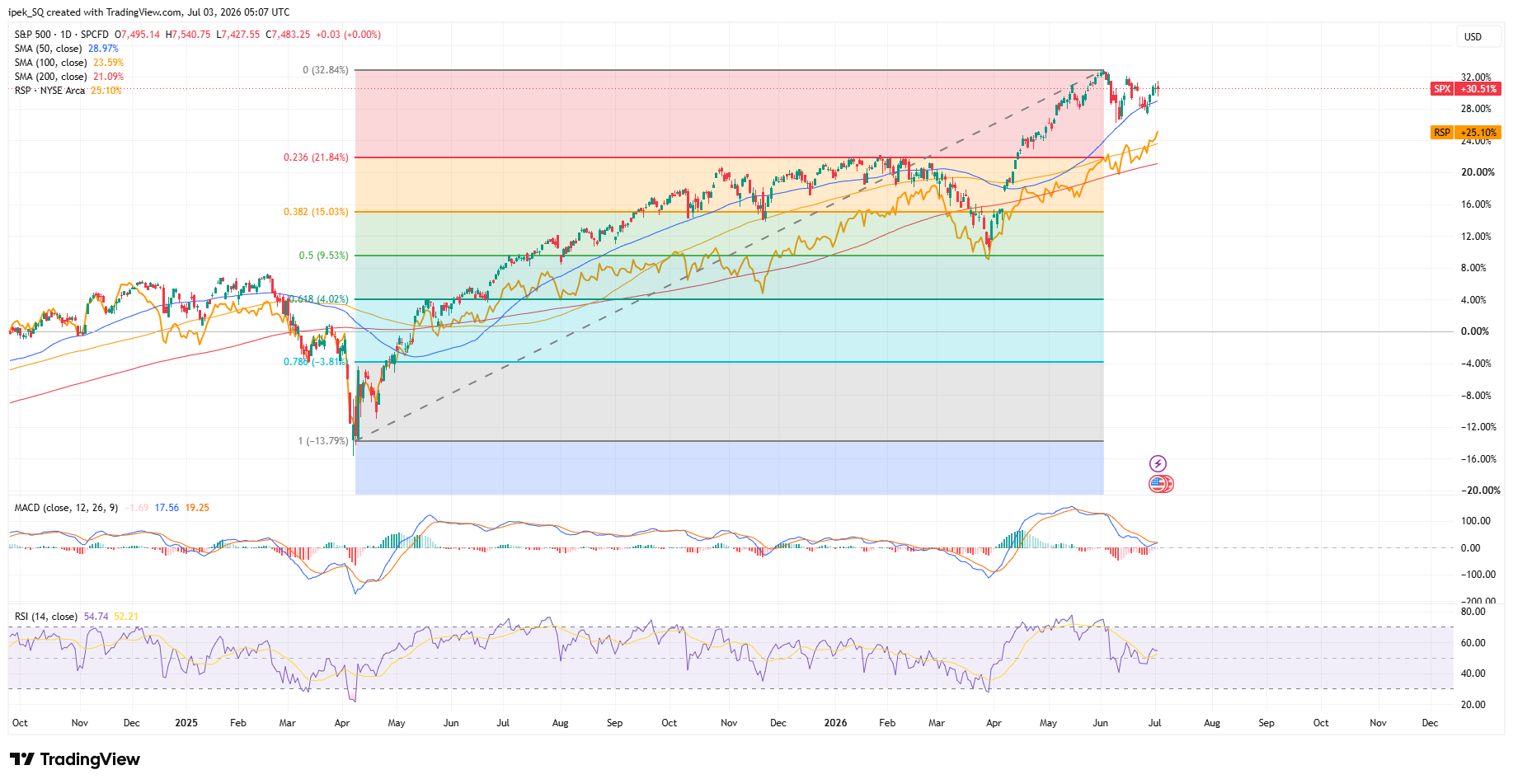

In equities, most companies in the S&P 500 reacted positively to the softer jobs data, which led to a notable decline in US yields. But the index closed the session flat as the selloff in technology—especially semiconductors—counterweighed gains elsewhere.

In this context, the tech-heavy Nasdaq 100 tanked 1.61%. In contrast, the Dow Jones Industrial Average rallied 1.14% to a fresh all-time high. The tech-poor Stoxx 600 and FTSE 100 jumped as well, with the former advancing to a fresh all-time high.

Futures are positive this morning, as softer Fed expectations are good news for everyone. The softer the Fed, the softer the dollar, the weaker the inflationary pressures stemming from dollar strength—and that is good news at a time when energy prices are falling.

Except for tech. Technology is dealing with its own demons. Chipmakers took a hit yesterday on news that Meta was stepping into the cloud business—a sign of potential excess capacity. Oracle also warned that some "highly leveraged" clients may fail to meet their obligations, pointing to risks around OpenAI.

Since then, however, reports suggest that OpenAI could give a 5% government stake (and keep relations hence regulation sweet), while Anthropic is reportedly in talks to develop a chip with Samsung. Samsung is up 9% today; in turn, the Kospi is preparing to close the session more than 5% higher, although it remains down more than 3% for the week.

The tech story will continue to dominate headlines, and tech appetite will likely be driven by industry headlines rather than macroeconomic factors. Yet further softness in inflation expectations—and therefore yields—could slow the tech selloff while directing capital toward less tech-heavy indices. Indeed, the equal-weight version of the S&P 500 is narrowing the gap with its tech-heavy, market-cap-weighted counterpart. I expect that trend to continue and help limit losses at the index level.

Until Elon Musks gets data centers into the orbit...

According to the latest environmental reports, Google and Amazon used a record amount of energy and produced a record amount of emissions due to the AI boom. In numbers, Google's electricity consumption jumped 37% compared with last year, while its water consumption soared 35%. Data centres were, of course, responsible for the surge in resource consumption. Amazon's greenhouse gas emissions rose 16%.

So, what’s striking is that market enthusiasm has been exceptionally strong for semiconductors, but nowhere near as strong for natural resources. Price action in oil and gas has been disrupted by the Middle East situation, clean energy-related assets gained momentum during the energy crunch but have been pulled lower following the reopening of the Strait of Hormuz, while uranium—and related assets—have been unable to maintain last year's positive momentum. The Global X Uranium ETF has lost almost a third of its value since its January peak.

It is becoming increasingly clear that if AI infrastructure continues to expand at this pace, demand for natural resources will keep rising—unless/until SpaceX eventually moves data centres into orbit, where abundant solar energy and the cold vacuum of space could dramatically reduce their energy and cooling needs. As such, assets related to natural resources (both traditional and clean) look under-owned.

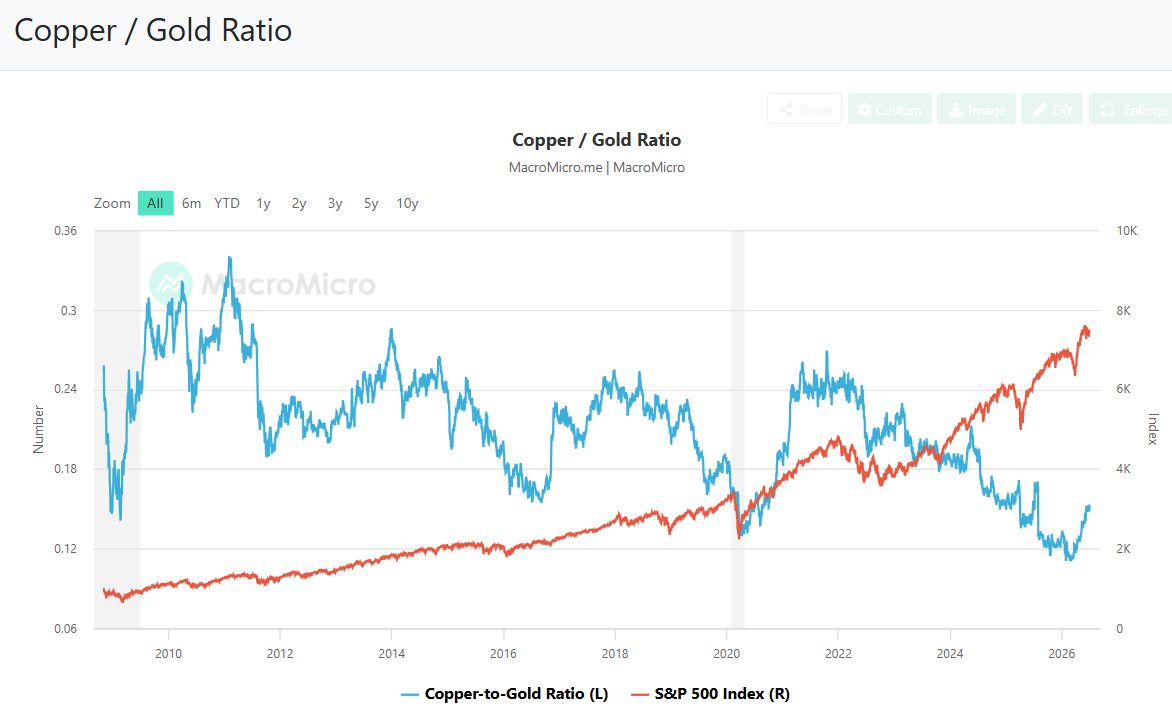

Copper, for example, has been in a strong and accelerating uptrend since mid-2022. Yet the copper-to-gold ratio has been falling steadily over the same period, overshadowed by gold's strong rally.

So when thinking about which pockets of the market could become the next beneficiaries of the AI boom, the energy and metals needed to power data centres deserve serious attention.

The content of this website is for informational purposes only and does not constitute financial advice. All opinions expressed are solely my own and should not be considered as recommendations to buy, sell or hold any financial instruments. Readers should consult a qualified financial advisor before making any investment decisions.

With love,

Ipek Ozkardeskaya