I was expecting to start this note talking about the US jobs data, the euro area inflation update and major central bankers’ latest thoughts about inflation and where monetary policy is headed (and I will get there), but instead, I will start with Meta’s decision to develop a cloud infrastructure business to sell access to computing capacity, chips and its AI models and continue with Oracle’s warning that AI investments may not turn into profits.

So, Meta is now willing to step into the cloud business, selling computing power, chips and access to its AI models, joining Microsoft, Amazon and Google in this area.

Meta jumped nearly 9% on the news, as investors were happy to see that the massive spending that looked to be going nowhere world-changing will finally end up in a potentially profitable business, but the news sounded alarm bells in my ears more than anything else.

- Meta has spent too much, eaten more than its stomach could take, and now needs to spit part of it out. It took debt on its shoulders along the way. It failed to release a go-to model, and it’s now moving to Plan B to make its investments worthwhile. Plan B will cost the company, so in theory, Meta is arguably in a worse place than the company itself thought it would be. I didn’t get why it rallied 9% on yet another failed business attempt.

- Meta is certainly not alone in the camp of those who spent too much on AI infrastructure. There could be other ‘cockroaches’. If that’s the case, we could see Big Tech slow down spending, and the latter would hurt the stellar future revenue expectations for the chipmakers that have gone ballistic over the past year. This is why we saw the Korean Kospi index sink more than 5% today.

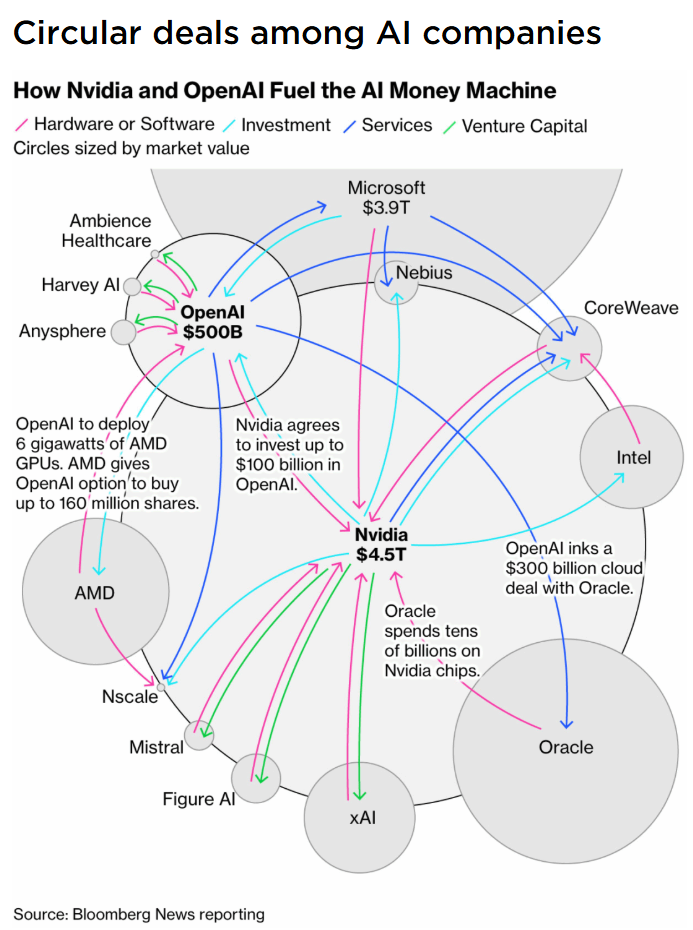

Second, Oracle disclosed parts of its annual financial report that came as an important warning – even though a less-than-3% selloff was nowhere close to reflecting the magnitude of what it said. The company warned that the construction of data centres may cost more and take longer than expected due to supply chain issues, government restrictions and third-party risks. OK. But more importantly, it warned that customers for whom the data centres are being built at this speed “may be highly leveraged” and “may experience risks of non-payment and non-performance in our dealings with such parties”. Here, Oracle is referring to customers such as OpenAI, which contracted massive computing power for years to come without any guarantee that future revenues will suffice to pay what it promised. In short, Oracle is saying that OpenAI may have ordered too much food, may not eat it all, and, worse, may not pay the bill.

And in the context of the AI ecosystem, where many of the best-performing companies have made big two-sided deals with each other – you invest in my company and I buy chips from you – such a misstep could have terrible consequences.

As such, the Nasdaq sold off 1.5% yesterday, with chipmakers leading the losses on fears that Big Tech may have spent too much and may slow its spending plans.

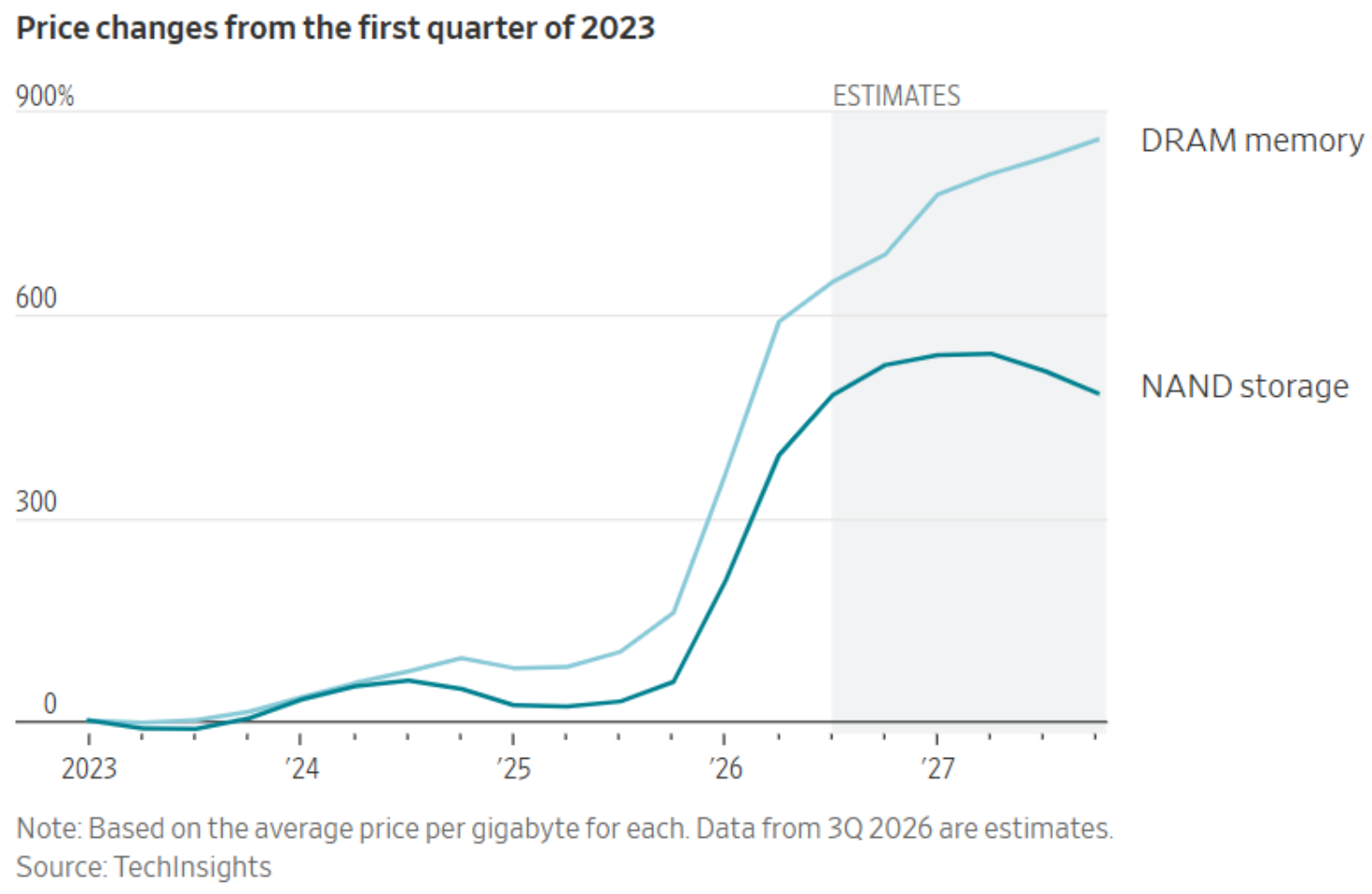

Oh, and the news that Apple is negotiating with blacklisted Chinese memory chipmakers to use them in devices sold in China added salt to the wound. China makes up around 15% of Apple’s sales and other companies could follow these steps as they also see their profits being squeezed by unreasonable jump in memory chip prices – we are talking about high triple-digit percent rise!

As such, Micron lost 10%, other chipmakers felt the heat quite notably, with the VanEck Semiconductor ETF falling more than 5%.

Then, the selloff hit neocloud providers such as CoreWeave and Nebius as well. Both printed double-digit losses (13% and 17%, respectively) in the session, while the S&P 500 closed with a much smaller 0.22% loss, as the majority of companies gained despite the bad smell.

Macro news encouraging

A further fall in oil prices on news that the peace negotiations are going well certainly helped. US crude fell nearly 3% to below the $68 per barrel level, as central bankers in Sintra sounded optimistic about inflation expectations. Both the new Federal Reserve (Fed) Chair, Kevin Warsh, and European Central Bank (ECB) President Christine Lagarde reckoned that the recent retreat in oil prices has had an easing impact on inflation – a development that could help them avoid further policy tightening in the coming months.

Cherry on top, the preliminary June euro area CPI data came in softer than expected. Headline inflation eased from 3.2% y-o-y to 2.8%, versus a retreat to 3.0% expected by analysts, while core inflation eased from 2.6% to 2.4%, versus 2.5% pencilled in by analysts. The EURUSD eased to 1.1361 and is sitting a touch above a key Fibonacci support – the major 38.2% retracement of the 2025–2026 rally (near 1.1350) – that should distinguish the euro’s year-and-a-half appreciation against the US dollar from a medium-term bearish consolidation zone.

The US dollar, on the other hand, strengthened across the board despite a soft ADP print (98K versus 118K expected, 122K prior) and a set of ISM numbers hinting at slower expansion in manufacturing but with softer price pressures as well – all giving the Fed doves reasons to enjoy the data. But no, the US two-year yield is holding a touch below the 4.20% mark as the US prepares to release its latest jobs data today before heading into the July 4 celebrations.

According to the consensus forecast, the US economy may have added around 114K nonfarm jobs in June, with monthly wage growth remaining steady at around 0.3%, while annual wage growth could edge up from 3.4% to 3.5%. Given the Fed’s explicit emphasis on inflation and price stability, any pickup in wage growth could revive hawkish Fed expectations and push US yields higher, pressuring equity valuations at a time when questions around the technology rally are getting louder.

The good news is that the reason inflation picked up momentum – the Iran war-led spike in energy prices – has largely faded. But the bad news is that if we see a correction in the technology complex, the rest of the index may find it hard to reverse the tide.

The content of this website is for informational purposes only and does not constitute financial advice. All opinions expressed are solely my own and should not be considered as recommendations to buy, sell or hold any financial instruments. Readers should consult a qualified financial advisor before making any investment decisions.

With love,

Ipek Ozkardeskaya