TSMC announced a record profit in Q2 and 77% profit growth compared with the same period last year. A 77% profit increase. The result was well above expectations, beating the already lofty consensus by nearly 12%. Yet the stock fell 5% after the earnings release.

Earlier this month, Samsung fell nearly 10% after announcing a 1’900% profit surge in Q2. That result also came in meaningfully above analyst expectations.

The inability of such impressive results to trigger a positive market reaction shows one thing: valuations across chipmakers have run ahead of themselves. These companies are not only priced to perfection, they are also increasingly priced in disconnect with the shifting AI outlook: people are growing uncomfortable with the massive AI buildout, pointing to overcapacity risks - among them is Federal Reserve (Fed) Chair Kevin Warsh, while investors growing uncomfortable with the industry's enormous AI spending, pointing to rising leverage risks.

Yet technology companies continue to spend. Alongside its 77% profit growth, TSMC sharply raised its revenue outlook and increased its capex guidance.

And it was precisely the latter — the higher capex guidance — that appeared to unsettle investors.

Ugly market reaction

Today, the Korean Kospi is not trading as South Korea is on holiday. But SK Hynix ADRs plunged 13% in the US session, while Nvidia fell 2.4% despite announcing a major deal with Japan, which plans to build a 140-megawatt data centre for its homegrown AI model for robotics. 140 megawatts is enough electricity to power roughly 100’000 to 140’000 homes, or a mid-sized city. Major Japanese groups involved in the project include SoftBank, Sony and Honda, while industrial names such as Fujitsu and Kawasaki Heavy Industries are also participating in the broader robotics and physical AI ecosystem. Yet SoftBank is down more than 12% this morning. And the Nikkei is diving 4%, with chipmakers leading the losses.

That tells us pretty much how the Korean Kospi would have reacted had it been trading today.

More on earnings...

Next week, Alphabet, Intel and Tesla will be among the major names reporting earnings. I can't wait to see whether they can turn the souring mood around. Alphabet was battered yesterday after reports that the latest update to its Gemini model would be delayed by several months. But I believe Alphabet's real winning trade is not its AI model; it is its data centres, TPU chips and its ability to monetise them. It should not, however, double down on infrastructure spending. Otherwise, TSMC's earnings gave us a good indication of how that news might be received.

Overall, besides the banks — which benefited, among other things, from financing the AI boom through stock offerings, bond issuance and IPOs — and energy companies, which profited from the Iran-war-driven energy crisis, this earnings season will not be a piece of cake.

Consumer-facing businesses will show how weakening consumer sentiment — and tariffs (which we tend to forget are still there) — have affected spending dynamics. The number of items sold at grocery stores fell nearly 2% according to Bain & Company, most likely due to sticker shocj and stretched household budgets, meaning that passing the higher energy prices on the clients becomes difficult – that means the profit margins will be taking the hit.

As for technology, the expected 63% earnings growth for the S&P500 tech companies could well be beaten. But even a comfortable earnings beat may not be enough to bring investors back if AI spending continues to run against investors' desire to see it contained.

To cut or not to cut?

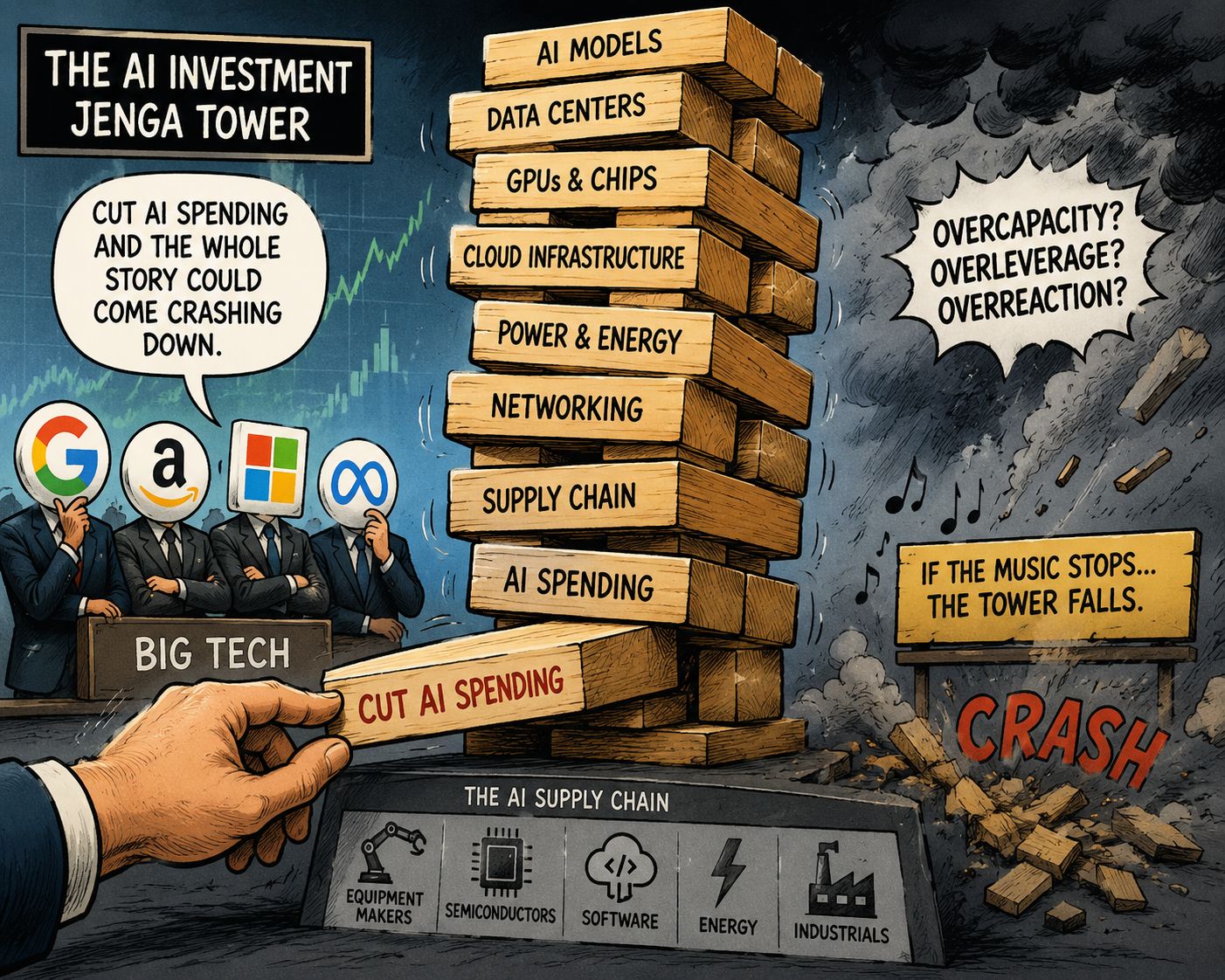

On the other hand, Big Tech knows that cutting AI spending would be like pulling a block from the bottom of a Jenga tower: it could bring the whole AI investment story crashing down. I wrote yesterday that the money flowing out of Big Tech is flowing straight into companies across the AI supply chain. So the question is: what happens when the music stops? And whether Big Tech would rather keep the music playing than hit pause altogether. It's starting to feel shaky.

What we know is that when frenzy fizzles out, it really fizzles out. Netflix, for example — one of the hottest stocks of the pandemic era that hardly anyone talks about anymore — fell nearly 10% after releasing its results yesterday. It has lost half of its value since June 2025. Netflix is no longer a market-moving stock, but it is certainly contributing to the negative mood in Nasdaq futures, which are underperforming their US and European peers heading into the European open. The final trading day of the week looks bearish.

Ugly geopolitics...

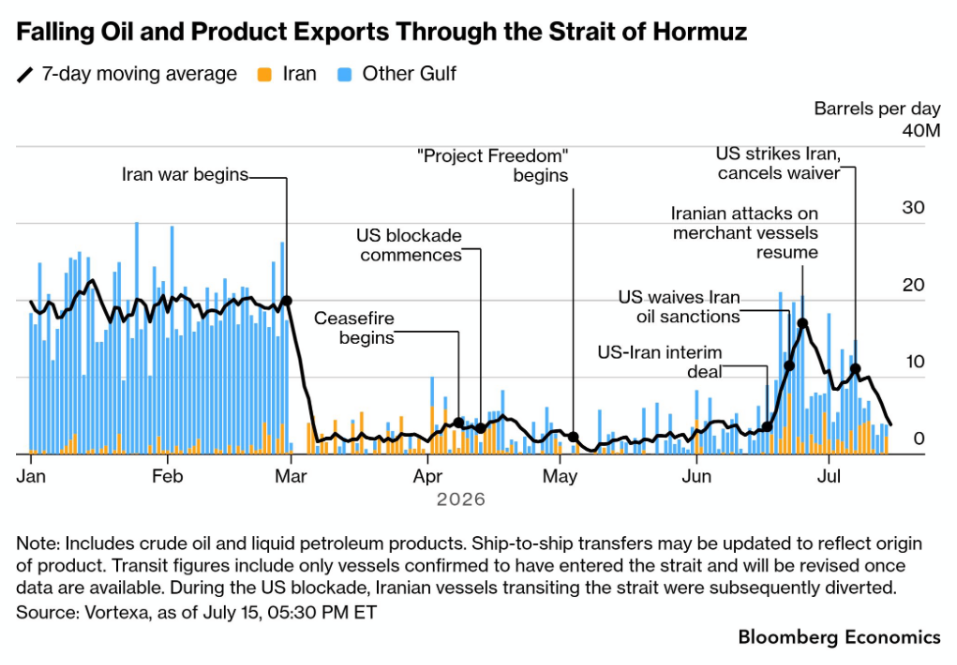

And the technology selloff is not the only reason markets are in a sour mood. Developments in the Middle East are getting worse by the hour. Traffic through the Strait of Hormuz has fallen to wartime levels. There is no easy resolution in sight, and the weekend could bring further escalation. All of that spells trouble.

The good news is that, so far, the reaction in the oil market has been more contained than during the early weeks of the Iran war. US crude continues to consolidate just below the $80-per-barrel mark, while Brent is holding near $85 per barrel. This relatively muted reaction is helping keep US Treasury yields under control. The US two-year yield, for example, has fallen for a fourth consecutive session, thanks to softer-than-expected CPI and PPI figures released this week. And that remains a critical factor for financial markets.

The good news is that, so far, the reaction in the oil market has been more contained than during the early weeks of the Iran war. US crude continues to consolidate just below the $80-per-barrel mark, while Brent is holding near $85 per barrel. This relatively muted reaction is helping keep US Treasury yields under control. The US two-year yield, for example, has fallen for a fourth consecutive session, thanks to softer-than-expected CPI and PPI figures released this week. And that remains a critical factor for financial markets.

The bad news is that we know the inflation relief cannot last if energy prices continue to climb. June's softer inflation was largely driven by lower energy prices. Those prices are now rising again.

In this context, in Europe — unlike in the US — the benchmark 10-year yield continued rising this week and briefly climbed above 3.16%, its highest level since the May peak, which itself was the highest since May 2011. That is not even helping the euro gain ground against the US dollar, which continues to benefit from safe-haven demand.

Meanwhile, the rotation out of technology continues to support the Stoxx 600, as financials and industrials absorb capital flowing out of the tech sector. Persistent upward pressure on yields could compromise that rotation trade in the short run. But investing is about identifying the next opportunity. Any pullback across markets will create opportunities to enter new positions at more attractive prices. And from today's perspective, the rotation toward financials and industrials still looks like the right place to be.

The content of this website is for informational purposes only and does not constitute financial advice. All opinions expressed are solely my own and should not be considered as recommendations to buy, sell or hold any financial instruments. Readers should consult a qualified financial advisor before making any investment decisions.

With love,

Ipek Ozkardeskaya