The technology stocks, especially those that spiked in a parabolic move, are being battered due to

1) their massive AI spending, increasingly financed by debt, with an unclear path to profitability for some of them, and

2) the prospects of higher interest rates that will increase the cost of debt in the months to come.

Note that the unease in US tech stocks started after the latest Federal Reserve (Fed) announcement, which came in more hawkish than expected, as the new Fed Chair Kevin Warsh put ‘price stability’ at the centre of his statement. The dot plot suggested that half of the Fed members are looking for at least one rate hike this year to tame inflation, which spiked above 4% last month for the headline figure and remains near the 3% mark for the core figure.

I highlighted that technology stocks have unusually outperformed their non-tech peers during the latest Fed tightening cycle thanks to the nascent AI boom and the ample free cash flow that Big Tech had at its disposal.

Since then, Big Tech has issued hundreds of billions of dollars worth of debt to finance its AI infrastructure, making these companies doubly vulnerable to the rate environment.

- Higher rates increase borrowing costs.

- Tech companies’ valuations are based on future revenues discounted back to today. Mathematically, higher discount rates weigh on valuations.

And well, it’s been a while that rising valuations have been calling for caution. AI-related infrastructure and services are certainly promising, but that promise has been very amply priced in – to stay polite.

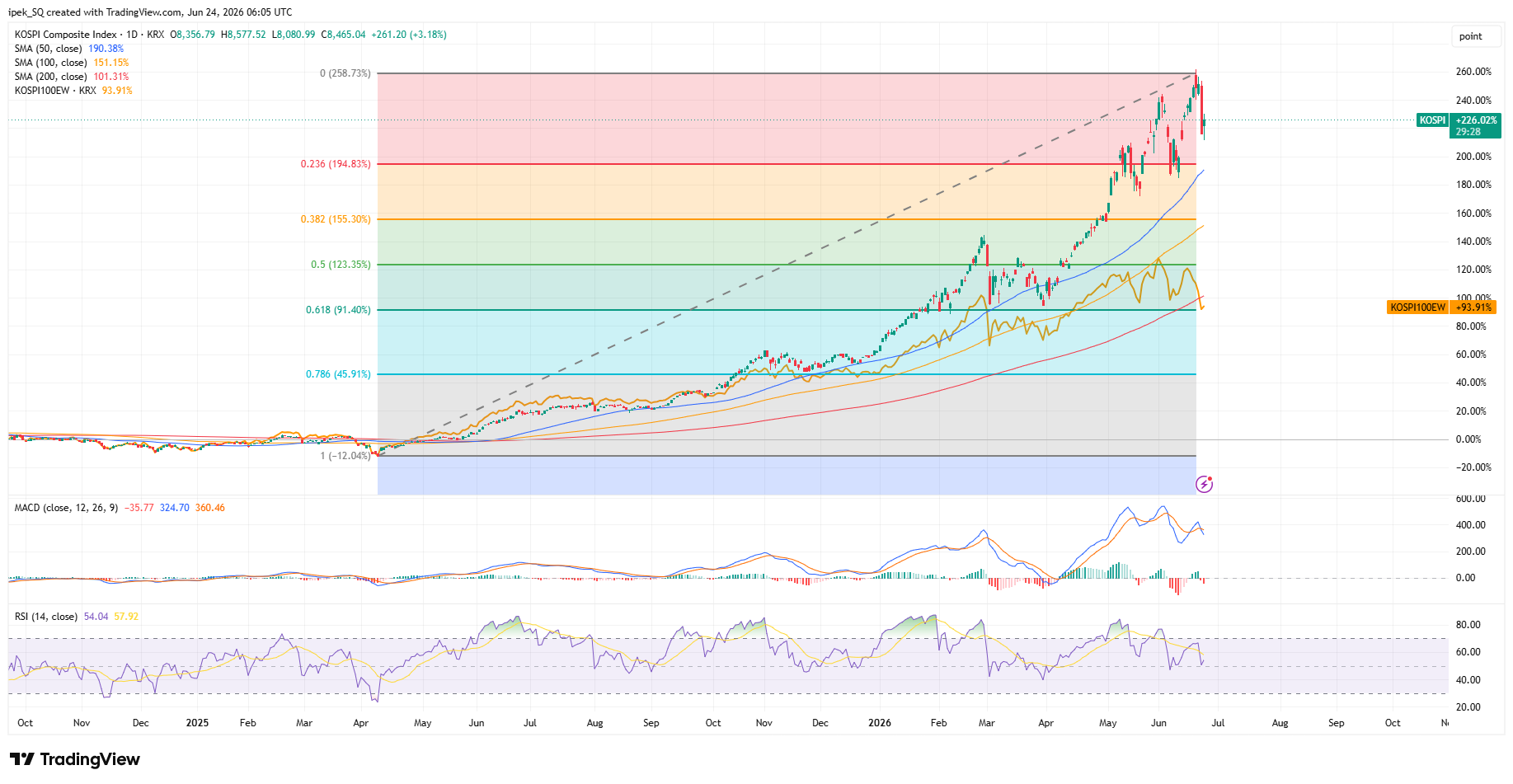

So the size of the drawdown is pretty impressive but totally understandable when looking at the preceding parabolic rally. The Korean Kospi index fell 10% yesterday – one of the biggest declines in its history – but it had rallied more than 300% since April 2025 on the back of two memory chip makers that found themselves in what is likely a prolonged boom cycle thanks to booming demand for high-bandwidth memory (HBM) chips used in AI accelerators and data centres. At one point, the two companies accounted for more than half of the index's gains and became increasingly dominant within the benchmark. Samsung’s P/E ratio went from below 10 for much of the past two decades to nearly 60!

In comparison, the Kospi’s equal-weighted index gained much less, as many Korean companies spent the past year simply trying to keep pace with a weaker won, rising input costs and sluggish domestic demand. Their earnings growth never matched the exuberance seen in the semiconductor sector, nor their attractiveness to global investors.

The Kospi was down when I sat down this morning and is now up by more than 2.50% on news that Samsung is considering buying back shares. But that does not change the underlying problem. A valuation this high and volatility this strong are never conducive to a healthy and sustainable trend.

In the US, the Nasdaq 100 tanked more than 3%. The hottest memory-chip stocks, such as Micron and SanDisk, both fell more than 13%, while losses across the Mag7 remained more contained at around 1.37%.

Futures are slightly higher this morning. But the reasons that triggered the recent unease have not gone away. The US 2-year yield is consolidating near its highest levels in one-and-a-half years, while a benchmark European 10-year yield is falling due to lower oil prices. US crude extended its retreat below $73pb this morning, limiting losses across European indices that are less exposed to technology and AI.

In this respect, the FTSE 100, for example, outperformed its European and US peers yesterday by closing the session near flat – and that despite a broad selloff in energy and mining stocks. Indeed, the bursting speculative bubble in metal prices has also halted miners’ parabolic surge. Fresnillo, a gold miner, has lost more than a third of its value since its January peak, while gold has fallen nearly 30% over the same period.

For precious metals, downside risks prevail as rising US yields increase the opportunity cost of holding non-interest-bearing assets. Whether gold could attract inflows in the event of a severe AI-led market meltdown remains to be seen.

Run or done?

So the question is: is the recent technology selloff the beginning of a potential AI bubble burst, or just another correction on the way up?

I don’t have the answer. But some stocks are screaming for a correction to return to healthier and more down-to-earth levels.

Today, Micron is due to release its latest quarterly earnings after the bell. Expectations are high. We will probably hear strong numbers and strong guidance.

But that is already priced in. Micron was trading above $1’200 a share two days ago, versus less than $120 a year ago.

The company’s trailing P/E ratio has surged to nearly 50x earnings – very high for a memory-chip business – reflecting the explosive growth expectations attached to the AI memory boom. Meanwhile, its forward P/E ratio is closer to 8–10x, implying that analysts expect earnings to surge over the coming quarters and bring the P/E ratio back down to more average levels.

But the gap between the two valuations is striking. It suggests that investors are not paying for today's earnings, but for tomorrow's expected profits, assuming that the current boom in high-bandwidth memory demand from AI data centres will be sustainable.

Very few are asking: what if it is not? What if new technologies – more efficient AI models, different chip architectures, etc. – reduce demand for memory?

That is why Micron's results matter far beyond the company itself. Strong numbers and confident guidance would reinforce the view that AI-related spending remains robust and could put a floor under the recent memory-chip selloff while supporting the broader semiconductor rally. But given the rich valuations across the AI ecosystem, anything less than spectacular could fail to justify the spectacular rise in share prices.

So the risk-reward is asymmetric, and it is a tricky time to release earnings.

Micron’s earnings – more specifically, the market’s reaction to those earnings – could influence the next direction for tech: run or done?

Again, some stocks are screaming for a correction to return to healthier and more down-to-earth levels, which could encourage further outflows from tech and trigger a rotation toward less richly valued, non-tech pockets of the market.

The content of this website is for informational purposes only and does not constitute financial advice. All opinions expressed are solely my own and should not be considered as recommendations to buy, sell or hold any financial instruments. Readers should consult a qualified financial advisor before making any investment decisions.

With love,

Ipek Ozkardeskaya