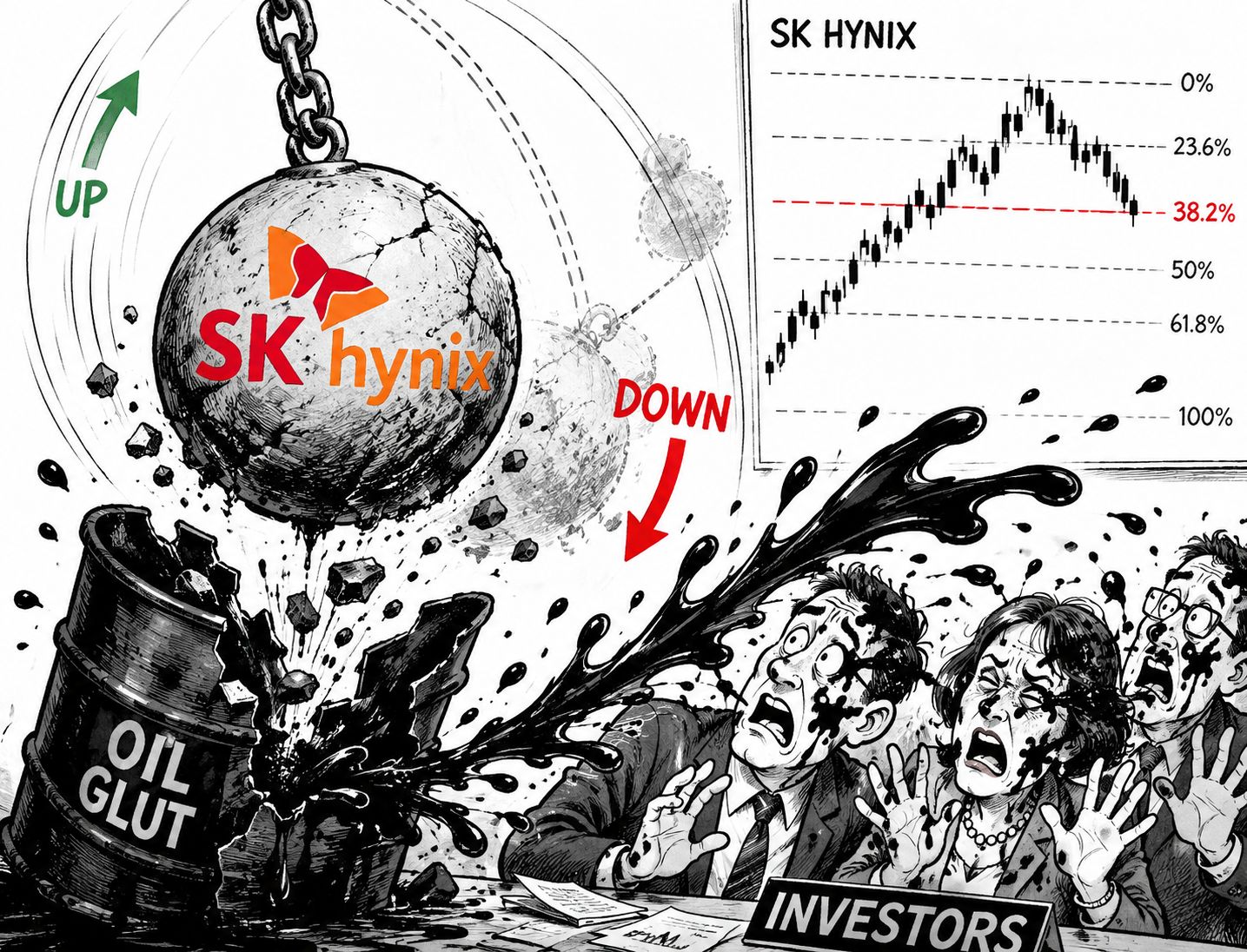

Last week ended with SK Hynix making history with a record debut in US trading for a foreign company. The stock rallied 13% on Friday as investors rushed to buy one of the hottest stocks of the moment on a US exchange, mainly because, even after last year's more than 1’700% rally, SK Hynix remains cheaper than some of its US peers. Its PE ratio stands near 18, versus Micron's, which currently trades at around 22.

Unfortunately, SK Hynix is down by more than 13% in Korea. From a technical perspective, it is now preparing to test a critical Fibonacci support level: the major 38.2% retracement of the April 2025 to June 2026 rally. This level should distinguish between a continuation of the positive trend and a medium-term bearish consolidation phase, which would point to a deeper downside correction.

The reason why this stock, along with other memory chip makers, has gone parabolic is that AI demand has somehow created the perception that a sector historically defined by boom-and-bust cycles could remain permanently in the boom phase. SK Hynix, since we're talking about the company, is planning to double its production capacity over the next five years to keep up with demand. The company's CEO says they would ideally need to increase capacity four- or five-fold, but he also admits that "he doesn't know" what the coming years will bring. Technological breakthroughs, more efficient AI models or simply a slowdown in AI infrastructure investment could quickly turn the market into one of oversupply.

That is the challenge. Because building semiconductor fabrication capacity requires years of investment, matching supply with demand is extremely difficult in this industry. Only time will tell when the two eventually meet, but one thing we can already say is that volatility in memory chip prices remains far too high to call the current price action sustainable. On the contrary, a quick glance to the price chart shows that a correction is already underway.

Earnings Season kicks off!

Of course, elevated stock market volatility is a boon for banks' trading desks, and we will see that reflected in a few days when the major US banks begin reporting second-quarter earnings. They are expected to deliver strong results thanks to higher market volatility, the SpaceX IPO and the higher-for-longer interest-rate environment. Consumer health remains a concern, especially as geopolitical tensions have re-escalated over the past week, but trading revenues and net interest income are expected to more than offset weakness on the consumer side.

Besides the banks, ASML and TSMC will also report earnings this week and will likely post strong results, supported by AI-related spending and robust semiconductor demand.

The real question is how the market will react.

Remember, last week Samsung lost almost 10% after reporting 1’900% profit growth for the previous quarter and has continued to fall since then. Therefore, investors' reaction to technology earnings may prove more important than the figures themselves. These stocks are still priced for perfection, yet several inconvenient truths are beginning to blur the picture.

- Spending remains exceptionally high and is eating into Big Tech's free cash flow.

- The hyperscalers are taking on more debt to finance AI investment.

- Investors are increasingly questioning the scale of AI capex and its eventual return on investment.

- Borrowing costs are rising at a time when geopolitical tensions are intensifying. And the Big Tech’s more leveraged balance sheets make them more vulnerable to interest rates today compared to past years.

That said, the S&P500 technology sector is expected to deliver year-over-year earnings growth of 63.3%, up from 62% last week and significantly higher than the 48.6% estimate at the end of March. Overall, S&P500 earnings are expected to grow by 23.6% in the second quarter, also up from last week's estimate of 22%. Expectations are high.

High expectations are also harder to beat.

Yet, looking at Big Tech, the second quarter was marked by a meaningful pullback in valuations. Google has retreated more than 16% from its May peak and is trading around 10% below its all-time high. Nvidia lost as much as 20% during the same period and remains roughly 10% below its own May peak, while Microsoft has lost more than a third of its value since October and is trading around 30% below its all-time high.

This means that Big Tech valuations have come down meaningfully, leaving room for a rebound in share prices if earnings prove strong enough.

Open or closed?

The weekend was anything but calm in the Middle East. The US continued its attacks on Iran, while Iran retaliated by attacking Gulf countries. The US says the Strait of Hormuz remains open to traffic, whereas Iran insists it is closed. That uncertainty is pushing oil prices higher this Monday. US crude is up more than 4% this morning.

Higher oil prices, in turn, are fuelling global inflation expectations and pushing bond yields higher. The US two-year Treasury yield, which best reflects expectations for Federal Reserve policy, climbed to its highest level since February 2025, while the Japanese 10-year yield recovered Friday's losses after Katayama called on the country's pension funds to invest more heavily in domestic assets. Remember — that's the horror movie scenario for global markets.

Higher bond yields are weighing on risk appetite. The Kospi is down more than 7%, while the Nikkei has fallen more than 3% in Tokyo. European and US equity futures are also trading lower.

Week Ahead

We are heading into a week packed with earnings, but also important macroeconomic data and events. Besides bank and technology earnings, investors will be glued to their screens for the latest US CPI figures as oil prices come under renewed upward pressure while hopes for a Middle East resolution drift further away.

Kevin Warsh will deliver his first semi-annual testimony before the US Congress. He is unlikely to say anything materially different from what he has already communicated. His priority remains fighting inflation, and he has repeatedly said he does not want to make assumptions or forecasts when so many of the factors influencing the outlook lie beyond the Fed's control. Can we blame him?

As a result, the US dollar will likely continue to follow oil prices higher (or hopefully lower!), while bonds and equities are likely to remain under pressure as long as oil extends rebound. Gold could test the $4’000 per ounce support level once again, although with limited conviction from the bulls to step in as rising bond yields reduce the yellow metal’s appeal. Defensive sectors are likely to attract inflows.

The content of this website is for informational purposes only and does not constitute financial advice. All opinions expressed are solely my own and should not be considered as recommendations to buy, sell or hold any financial instruments. Readers should consult a qualified financial advisor before making any investment decisions.

With love,

Ipek Ozkardeskaya