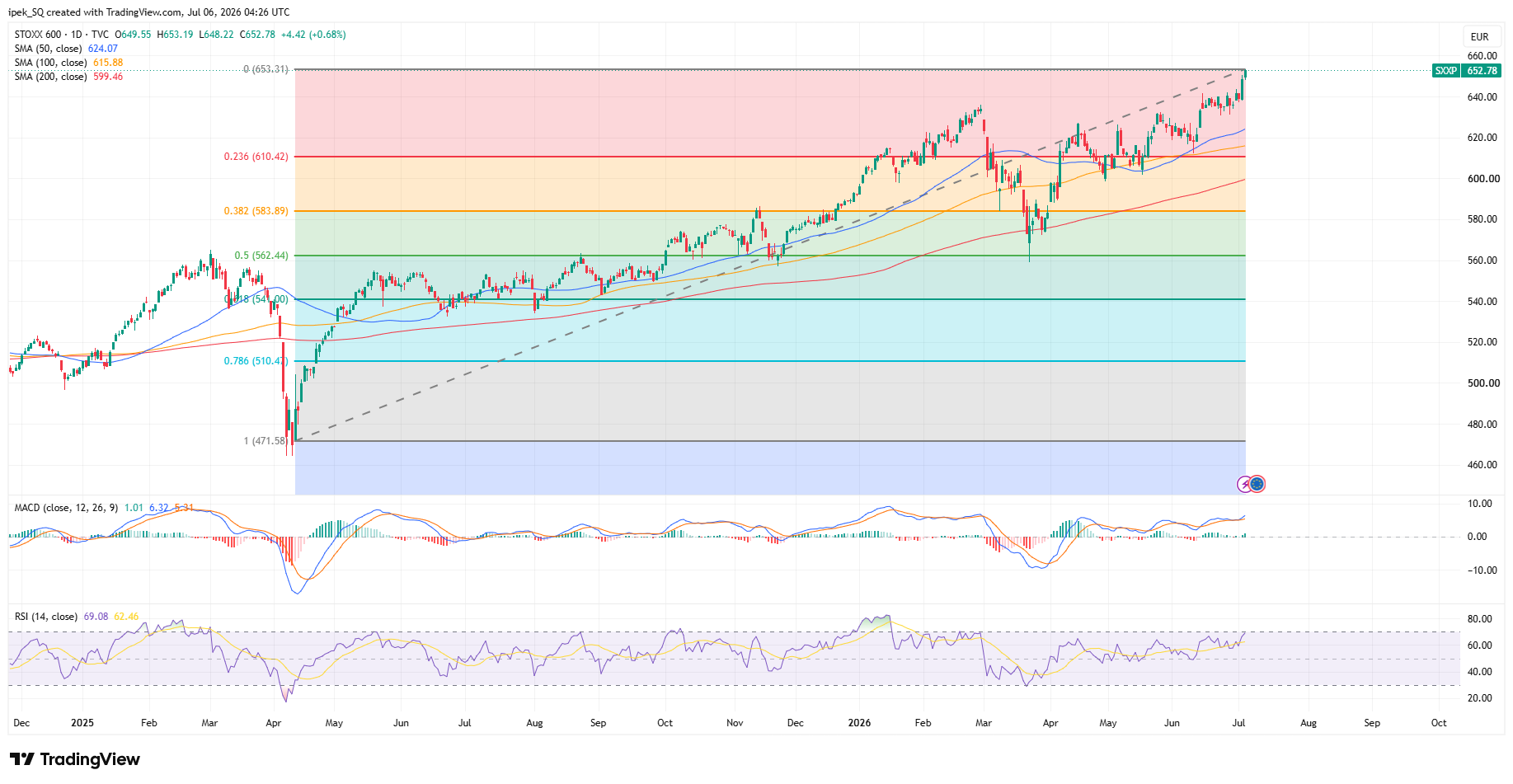

Last week ended on a positive note for European equities, as US markets were closed for the July 4th holiday. The Stoxx 600 advanced to a fresh record high despite a slight rebound in bond yields after Friday’s PMI data showed stronger-than-expected activity in June, especially in services, perhaps helped by sunny weather and the World Cup. The FTSE 100 is also approaching its own ATH levels – reached back in February – despite falling oil prices and downside pressure on mining stocks.

Speaking of oil, Friday’s data showed that several OPEC+ producers increased production, and the group also announced that it would raise output by 188K bpd, further unwinding the restriction strategy put in place back in 2023. The increase won’t materially change global supply, but it comes at a time when supply-glut talk is resurfacing, pulling oil prices lower (along with the Middle East de-escalation), and after the UAE quit OPEC, hinting at an upcoming battle for market share rather than cartel-boosted profits. US crude is consolidating near $68.50pb this morning, despite some jittery news in the Strait of Hormuz suggesting that some tankers made U-turns, but eventually crossed the Strait.

So, the new week starts on a mixed note. European futures are pointing to a cautious start, while tech-heavy US futures are leading gains before the European open, despite mixed sentiment toward tech in Asia. The Korean Kospi, for example, is slightly sold off – though recovering losses at the time of writing – after news that Samsung would increase the prices of its memory chips by another 20%. Remember, high triple-digit percentage rises in memory chip prices have started to squeeze profits at hardware makers, making the demand outlook cloudier for memory chip makers and investors anxious and undecided about whether the news is good or bad. Samsung initially jumped but gave back gains, and is up by around 0.80% at the time of writing. SK Hynix, which is preparing to list in the US this week to tap deeper US financing, starts the week more than 3% down. The company’s PE ratio is around 21.50, versus 21.90 for Micron. To me, and after a more than 1700% rise in a bit more than a year, I am curious to see how much juice the company can squeeze out of US markets at a time when bubble worries are getting louder and taming appetite.

Another piece of good news came from Hon Hai Precision, also known as Foxconn, Apple’s main iPhone assembler and a key manufacturing partner for Nvidia’s AI infrastructure. The company reported an almost 40% jump in quarterly sales, beating estimates, but its share price barely reacted to the news.

SpaceX in Nasdaq 100

This week, investors will continue to question technology valuations: whether they have gone too far, whether they make sense, or whether this is another great bubble – like railways or dot-com – waiting to burst, while watching SpaceX enter the Nasdaq 100 index. Remember, Nasdaq changed the inclusion rules to include SpaceX, which would normally not make its way so quickly into such a broadly watched and traded index, given its extremely low free float, its governance – Elon Musk has more than 80% of voting rights – and its fundamentals, as the company went public at a valuation of more than 100 times last year’s sales. Needless to say, SpaceX’s inclusion will increase the Nasdaq 100’s volatility, challenge its capacity to represent underlying economic and financial fundamentals, and potentially hurt its credibility.

This week also marks the end of the quiet period for SpaceX, meaning that Wall Street firms will start publishing their first research reports. From a stock-price perspective, the early enthusiasm faded fast, with the price coming close to its IPO level after a more than 50% surge in the early days.

Elsewhere

Some consumer-facing companies including PepsiCo and Levi’s will report earnings, and the FOMC will release the minutes of its latest meeting, where the new Federal Reserve (Fed) Chair Kevin Warsh put emphasis on ‘price stability’ and refused to include his projections in the dot plot, arguing that forward guidance and Fed members’ frequent comments had gone too far, suggesting a change in the Fed’s communication strategy and its too-close relationship with markets.

Even though falling oil prices have tamed inflation expectations so far, markets still price in one rate hike from the Fed in the second half, and the hawkish shift continues to support the US dollar. The USD index is well bid against most majors this morning, with the EURUSD consolidating recent losses below the 1.15 mark and the USDJPY starting the week with another leg up after Goldman revised its 12-month forecast from 155 to 165.

What’s notable is that the yen’s weakness is due to abnormally low Bank of Japan (BoJ) rates and a very large yield gap with other DM peers. But low rates don’t necessarily help Japanese companies perform well. In fact, Japanese bankruptcies are very high due to the undesirable effect of the weak – and weakening – yen. In this context, the BoJ had better raise rates and normalise policy to give relief to the Japanese economy, which can’t fully enjoy low rates. If that happens, though, Japanese investors could repatriate funds to Japan and pull the rug from under the feet of global markets, which have benefited from ample Japanese funds for decades. Alas, abundant liquidity has been enough to tame reverse carry trade worries since Japan's 10-year government bond yield broke above the 1.70–1.75% range last November — a range once feared as the trigger for a reverse carry trade. Today, Japan's 10-year yield is at 2.80%, the highest in decades and still rising, yet no one seems to care.

And it's generally when you expect it the least that markets deliver their nastiest surprises.

The content of this website is for informational purposes only and does not constitute financial advice. All opinions expressed are solely my own and should not be considered as recommendations to buy, sell or hold any financial instruments. Readers should consult a qualified financial advisor before making any investment decisions.

With love,

Ipek Ozkardeskaya