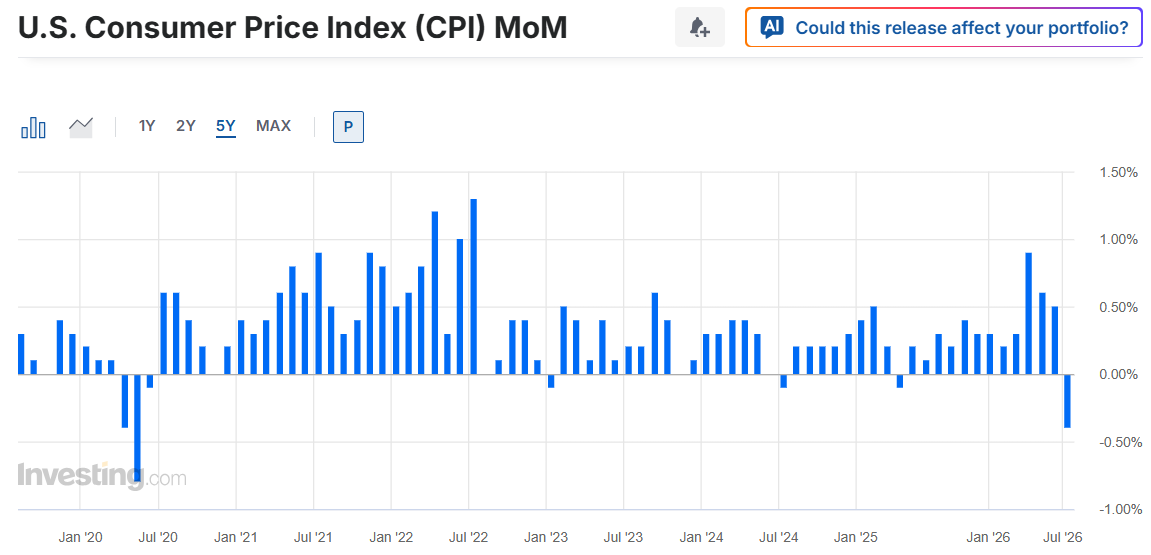

US inflation came in softer than expected yesterday. But not only that. The monthly figure printed a negative reading – the most negative in six years. The biggest explanatory factor was the fall in energy prices. As mentioned yesterday, US crude fell around 25% in June, pulling US gasoline prices down by around 10%, and the latter was clearly reflected in the data.

Looking at the yearly figures, headline inflation sank from 4.2% to 3.5%, well below the 3.8% expected by analysts, while core inflation eased from 2.9% to 2.6%, also notably below the 2.8% pencilled in by analysts. In fact, the core figure fell back to pre-Iran war levels.

To my surprise, the data tamed hawkish Federal Reserve (Fed) expectations, leading to a sharp pullback at the short end of the US yield curve. The US two-year yield, which best captures Fed rate expectations, fell 10bp. Activity in Fed funds futures is now pricing the probability of a September rate hike at 60%, down from 77% before the CPI release.

But because the drop in US inflation was largely driven by the sharp pullback in energy prices, the inflation relief will probably not last long. Middle East tensions are escalating. The US President walked back his latest – and perhaps one of the most absurd proposals yet – to charge a 20% fee on all ships transiting the Strait of Hormuz (we did the math yesterday: it would amount to a $30–34 million fee per oil tanker and would be against international law). Yet strikes in the region continue, energy infrastructure is being damaged, and oil and gas prices are rising. US crude is consolidating its rebound near $80pb, Brent is trading near $85pb. NYMEX natural gas remains stable below $3, yet European TTF futures are up more than 30% since the June dip.

In summary, the good news on the US inflation front is unlikely to last. This is why I was surprised by such a positive market reaction.

Fed Chair Kevin Warsh himself rightfully downplayed the latest inflation data and said – loud and clear – that there would be "no tolerance" for high inflation.

Overall, June's inflation data offered a brief painkiller for the markets. It helped mask the symptoms, but the disease is still there. Oil prices will remain central to inflation dynamics and, therefore, to central bank expectations.

Besides that, Kevin Warsh also said that he doesn't want to be in the bailout business if anything goes wrong in the markets, although the Fed would still be there to provide support. Whatever that means.

Soft CPI fuels bulls, banks & tech lead gains

US futures are in positive territory this morning, while European peers point to a weaker open, weighed down by the rebound in energy prices. The divergence between the US and Europe seems to be driven mainly by technology stocks, which are outperforming again today, with the Kospi adding another 7.70% at the time of writing, while ASML's results also came in sweet, accompanied by higher-than-expected guidance for both Q3 and full-year sales. We will see how investors react throughout the day.

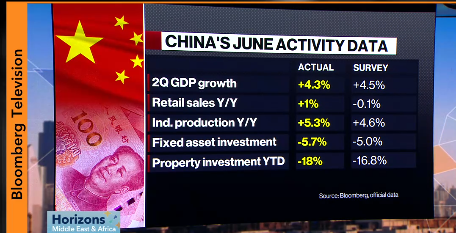

Over in China, the mood remains cheerful despite a mixed set of economic data showing softer-than-expected second-quarter GDP growth, a further decline in investment and property prices, alongside relatively stronger retail sales and industrial production, as the country's exports continue to boom thanks to robust demand for AI hardware and cheaper AI tokens. According to the latest news, DeepSeek is now looking to go public as early as this year.

Back to earnings, ASML was not the only company to deliver good news.

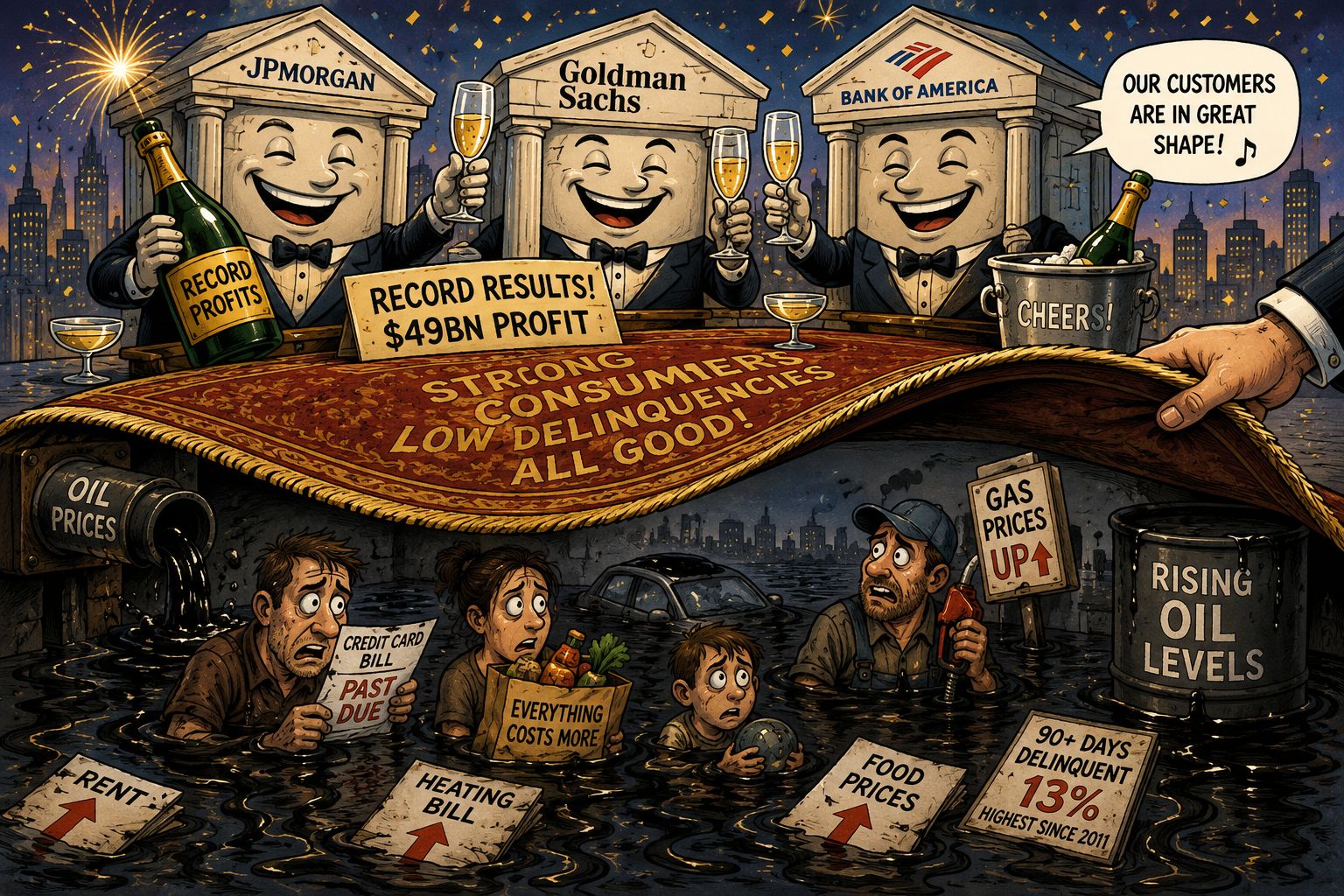

US big banks kicked off the earnings season with a bang yesterday. JPMorgan, Goldman Sachs and Bank of America all reported record trading quarters amid elevated market volatility and a strong IPO market (yes, I am talking about SpaceX, which, by the way, is now heading straight down as investors realise the company will have to spend heavily – perhaps for many years – to achieve an ambitious dream).

Together, the biggest US banks generated a record $49 billion in second-quarter profits and said consumers remain in good health despite rising energy prices and heightening inflation concerns. And not just wealthier customers, according to JPMorgan's CFO, but broadly across the bank's customer base.

CEO Jamie Dimon says, "it's getting close to as good as it gets."

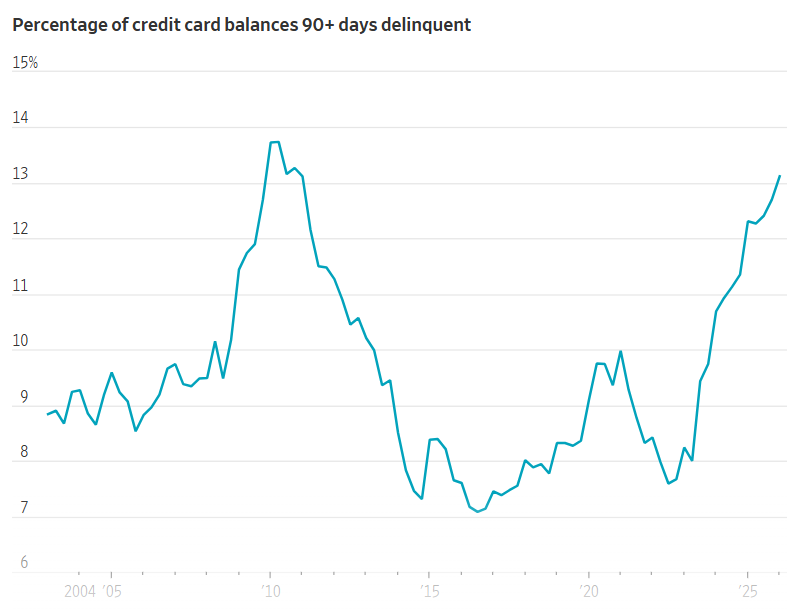

Funny enough, these numbers stand in stark contrast to the exploding share of credit card balances that are more than 90 days delinquent. According to the latest data, that figure has climbed above 13% – the highest since 2011.

Source: WSJ

Source: WSJ

It seems the biggest banks' customer base isn't quite Main Street enough to reveal the dust that's quietly building up under the rug.

The good news is that the strong bank results did trigger a positive market reaction. Invesco's KBW Bank ETF gained 1% yesterday to a fresh all-time high, tracking the big banks' record profits. Financials have been outperforming the S&P 500 since June, and the ongoing rotation away from richly valued and volatile technology stocks could continue to benefit the sector.

For IBM, earnings day didn't go nearly as smoothly. The stock plunged more than 25% – apparently its worst sell-off since 1968 – after the company acknowledged that it had misread the AI trend by underestimating the "magnitude of the capex reprioritisation" and by being "distracted" by cybersecurity needs. Money, meanwhile, continued to flow into chipmakers, semiconductor equipment companies and AI tokens, leaving software behind.

The good news is that IBM's misery didn't spill over into the broader software sector. The iShares Expanded Tech Software ETF still managed to eke out a 1% gain, suggesting that stress among software investors is easing and leaving the sector with plenty of room for a recovery. Good earnings could certainly help after the industry's severe sell-off between last September and this April.

Today...

Zooming out again, today the US will release the latest PPI data. Headline PPI is expected to have eased from 6.5% to 6.2%, while core PPI may have accelerated from 4.9% to 5.2%. Either way, these figures remain far too high relative to the Fed's 2% inflation target and could bring investors back down from yesterday's rosy cloud to the much greyer reality of rising Middle East tensions and a conflict that is far from being settled.

The content of this website is for informational purposes only and does not constitute financial advice. All opinions expressed are solely my own and should not be considered as recommendations to buy, sell or hold any financial instruments. Readers should consult a qualified financial advisor before making any investment decisions.

With love,

Ipek Ozkardeskaya